The main objective of a retirement portfolio is to provide an income that assures you a standard of living similar to or better than the one you enjoyed while you were fully employed. The goal is to meet your cash flow needs while maintaning capital preservation. Other objectives may include maintaining appropriate health insurance coverage and minimizing both your income and estate taxes.

A retirement portfolio can have the following components: Pension, 401(k), IRA, stocks, bonds, mutual funds, certificates of deposit and treasuries, real estate, and social security income.

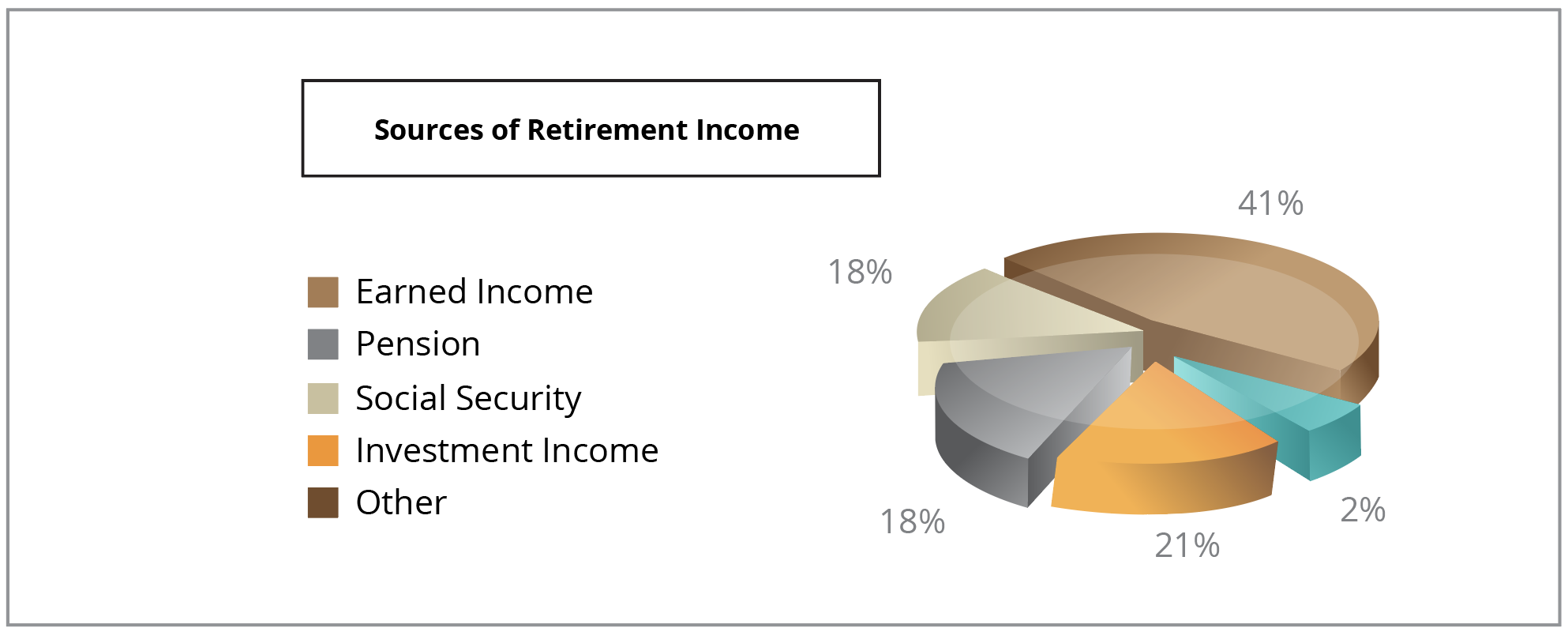

StateTrust's financial advisors have the expertise and qualifications to build efficient retirement portfolios to meet individual client needs. The image below shows sources of retirement income in the United States as of 2010.

A Retirement Plan

We can assist you in setting up a thorough retirement plan that provides investment solutions that fit your goals and risk tolerance levels. The following are some important points to take into account:

- Prioritize your retirement goals.

- Determine your income needs.

- Identify issues and opportunities.

- Recognize and manage retirement risks.

- Monitor and update your strategy.

StateTrust combines retirement and investment solutions depending on the needs of each individual. We provide a sound strategy that takes into account a long-term retirement plan, including portfolio allocation adjusments as the client's retirement period is approached.

- Diversified Retirement Assets: Client portfolios are diversified across major assets classes and sub-classes (asset allocation will depend on client's time horizon, risk tolerance levels, and investment goals).

- Re-allocation: It depends on the financial needs and expectations of our clients.

- Expert Guidance: StateTrust Investment Advisors help clients build these portfolios, select an appropriate strategy, re-balance the assets, and review performance.

Retirees face several risks

Retirees are being confronted today by challenging situations that put their retirement plans in peril and can affect their peace of mind post-retirement.

StateTrust develops investing strategies to deal with the following retirement issues:

- Living longer: Outliving a retirement portfolio is a concern (especially given advances in medicine) for those who decided on an early retirement or for those who have a family history of longevity.

- Market Volatility: It makes client portfolio values fluctuate, potentially affecting the income clients need to maintain their lifestyle level.

- Spending: Clients need to understand post-retirement expenses and what level of income they need to keep their pre-retirement lifestyle.

- Social Security/Pensions: Social Security and pension plans might not yield the same benefits in the future given the current debt/entitlement crisis.

- Savings: Saving enough money for retirement is a difficult task and requires a consistent approach to savings.