StateTrust is a recognized leader in serving the financial needs of individuals and families with asset management and global wealth management solutions. Our Investment Advisors are ready to help clients meet their investment needs by providing a complete range of mutual funds and investment solutions.

A mutual fund is a professionally managed collective investment security that pools money from many investors and invests typically in a pool of investment securities (stocks, bonds, short-term money market instruments, other mutual funds, other securities, and/or commodities such as precious metals). The mutual fund will have a fund manager that trades (buys and sells) the fund's investments in accordance with the fund's investment objective.

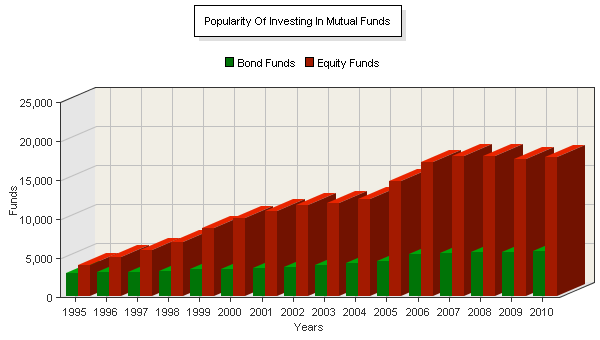

The number of mutual funds has grown dramatically over the last decade, with more than 24,000 funds now available.

<!--

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.-->

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.-->

Advantages of Mutual Funds

Among the advantages of Mutual Funds are:

- Simplicity - Investors with limited knowledge, time or money can invest in multiple securities.

- Professional Management - Having third party professional fund managers apply their expertise and time to manage and research investment options.

- Diversification* - Instant diversification, asset allocation and risk reduction without the large amount of cash needed to create individual portfolios.

- Economies of Scale - Fund managers obtain lower transaction fees from a large pool of purchases.

- Liquidity - Ability to sell with relative ease in a short period of time without there being much difference between the sale price and the most current market value. However, it is important to be aware of any fees associated with selling, including back-end load fees. Mutual funds transact only once per day after the fund's net asset value (NAV) is calculated.

* Diversification does not guarantee a profit or ensure against loss.

Mutual Fund Investment Categories

Mutual funds are often categorized by their investment objective or the assets in which they invest.

- Domestic Stock Mutual Funds - These mutual funds invest in several categories of domestic stocks.

- Large stocks (generally with a market cap over $10 billion) are comprised of established companies.

- Small stocks have low market capitalization (generally less than $1 billion) and are typically more volatile than large stocks.

- Growth stocks belong to companies with earnings that are expected to grow quickly, while value stocks have low prices relative to earnings, book value, or cash flow.

- Specialty stock funds invest primarily in securities of a particular sector, industry, or region.

- Target-date funds combine stocks and bonds, and their asset allocation grows more conservative as the fund approaches the target date.

- International Stock Mutual Funds - World-stock funds invest in equities throughout the world, including U.S. stocks. Foreign-stock funds invest primarily in worldwide equities traded outside the U.S. Foreign securities involve special risks that investors should consider, such as fluctuations in currency, foreign taxation, political instability, and differences in accounting and financial standards. These funds can invest in small, medium, and large companies with growth or value characteristics. A regional fund restricts its investments to securities in a particular geographical region, while emerging-market funds invest in financial markets of developing countries.

- Bond Mutual Funds - A number of available mutual funds focus on bonds. U.S. government bonds are issued by the Department of the Treasury, while corporate bonds are issued by corporations. Municipal and state general obligation bonds are issued by state and local governments. Municipal bonds are exempt from federal taxation*. Short-term, intermediate-term, and long-term bonds are classified by their term to maturity. The quality of the bond depends on the issuer's ability to repay the bond in time.

- Money Market Mutual Funds - Money market funds represent investments in short-term, high-quality securities such as Treasury bills and certificates of deposit (CDs). These funds are less volatile than stocks or bonds and are highly liquid. An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although money market funds seek to preserve the value of your investment at $1 per share, it is possible to lose money by investing in these funds.

* Income maybe subject to the Alternative Minimum Tax (AMT)

Mutual Fund Share Types

Mutual funds can also be classified by their fee structure into three broad share class categories: A, B, and C. The share class generally indicates the fees associated with investing in a particular mutual fund. Investors can select a fund share class that is best suited to their investment goals.

| Share Class | Description |

|---|---|

| "A" Shares | Class A shares charge a front-end sales fee and are often an attractive choice for investors seeking to invest a large amount of capital for a long period of time. A shares offer discounts on the front-end sales charge, also known as breakpoints, to investors willing to invest in excess of a certain dollar amount. Fees associated with this share class tend to be lower than B or C shares |

| "B" Shares | Class B shares do not have any front-end sales charges. They do, however, charge a contingent deferred sales fee that declines over time. Fees associated with this share class tend to be higher than A shares. At the end of a seven- or eight-year time period, B shares typically convert to Class A shares. |

| "C" Shares | Class C shares are exempt from front-end charges and usually include a lower contingent deferred sales charge than B shares. Unlike Class B shares, fees do not decrease with the passage of time and C shares do not convert to A shares. |

Evaluating Mutual Fund Style

Style analysis is an analytical technique used to understand investment style and identify the characteristics of a fund or portfolio. The two principal methods of style analysis are holdings-based style analysis and returns-based style analysis.

- Holdings-Based Style Analysis

Holdings-based style analysis classifies funds based on characteristics, such as size (small, mid, large cap) and value/growth orientation, of the underlying securities. Holdings-based style analysis may help identify style drift and attribute performance to a sector or stock selection. One limitation to holdings-based analysis is that it is subject to the reported holdings at month or quarter-end when fund managers may be investing elsewhere intra periods (this is often called “window dressing”). The goal of holdings-based style analysis is to explain the composition of a portfolio.

- Returns-Based Style Analysis

In contrast, returns-based style analysis compares the total returns of a fund to the total returns of a set of benchmarks over a period of time. This type of analysis accounts for the behavioral characteristics of the asset, but does not analyze the actual holdings. Returns-based style analysis uses a set of weights that represent the average exposure of a fund to various asset classes over a period of time. One limitation of this type of analysis is that it is only as meaningful as the relevance of the benchmark set. The goal of returns-based style analysis is to provide insight on how a portfolio has behaved.

Mutual Fund Fees

There may be a percentage charge levied on the purchase or sale of shares or 'front-end load'/'back-end load'. This charge may represent a profit or cost coverage to the fund manager for the distribution, commissions, advising and brokerage that arranged the purchase and/or sale. These fees are commonly referred to as 12b-1 fees in the U.S. Not all fund have initial charges; if there are no such charges levied, the fund is "no-load".

Net Asset Value

Mutual Funds are priced by Net Asset Value or ("NAV"). This is the price per share, calculated by dividing the fund's assets minus liabilities by the number of shares outstanding. This is usually calculated at the end of every trading day.

Glossary of Mutual Fund Terms

| Term | Description |

|---|---|

| Asset-Based Sales Charges | These are fees you would not pay directly, but which are taken out of a mutual fund's assets to pay to market and distribute its shares. |

| Breakpoint Discounts | Discount offered on the front-end sales charge if you: make a large purchase, already hold other mutual funds offered by the same fund family or commit to regularly purchasing the mutual fund's shares. |

| Closed-End Fund | Money can only be raised in a single offering, much the way a stock issue raises money for the company only once, at its initial public offering, or IPO. |

| Contingent Deferred Sales Charge |

Fee charged when you sell your mutual fund shares. |

| Expense Ratio | A measure of the fund's total annual expenses expressed as a percentage of the fund's net assets. |

| Front-End Sales Charge |

Fee charged when you purchase mutual fund shares. |

| Open-End Fund | investors can buy and sell shares at any time. |

| 12b-1 fees | Marketing and distribution Fees. Capped at 1 percent of your assets in the fund, these fees are taken out of the fund's assets to pay for the cost of marketing and selling the fund and some shareholder services. |

Links of interest: