Having the means to enjoy a financially secure retirement is the key goal of retirement planning. And while there are other considerations in the interim before retirement—demands such as purchasing and maintaining a home, paying for college, medical expenses, insurance premiums, and income taxes—it is essential that you take the time to plan for your retirement carefully.

In order to reach a financially secure retirement, it is necessary to have the advice, tools and products needed to reach your retirement financial objectives. StateTrust has the experience, knowledge and personnel specializing in effective strategies to achieve your retirement financial goals.

Building up the assets necessary to achieve a financially secure retirement requires systematic savings over time and a professional investment methodology.

StateTrust has the experience and technological resources to establish a plan, based on your assets, liabilities, income and investment returns, that will help you achieve a successful retirement.

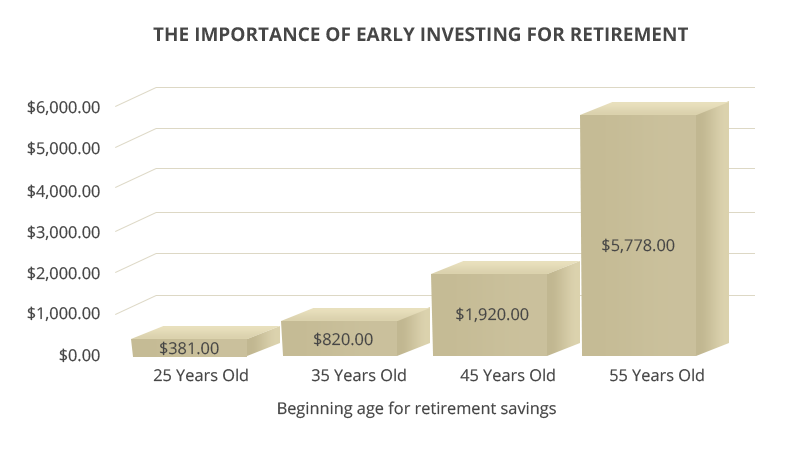

- The sooner you can get started on your retirement plan, the less you will need to save to meet your financial goals. This is due to the compounding effect of investment returns. The graph below shows the monthly savings amount necessary starting at a particular age to reach $1 million at age 65.*

- Retirement planning/saving can start at any point before retiring, but it is recommended to begin planning/saving at least 15 to 20 years before exiting the workforce.

- A longer interval of time means there is a greater possibility of effectively handling unexpected changes such as medical expenses, a big increase in inflation, the loss of a loved one, sharp fluctuations in the market and natural disasters.

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.

For our clients in the United States, we offer a multitude of investment options, from traditional Individual Retirement Accounts (IRAs) to 401 (k) plans for corporations and their employees.

If you are a United States client, you can use the links to the right to view different types of retirement accounts.

For Our International Clients

StateTrust has developed an extensive international clientele, in dozens of countries and multiple continents. Our management team is attuned to the needs and issues that can be present for international clients. Our international clients can take advantage of a number of programs customized to meet their retirement needs.

- Our international advisory unit will help you establish the risk/return characteristics of investments needed to meet retirement goals.

- Investment recommendations will take into account specific jurisdictional issues including asset ownership structure and residency status of you and your beneficiaries.

- Asset allocation and portfolio design will encompass tax optimization strategies .

- We have developed an international alliance program which include strategic partnerships with accountants, attorneys, custodians, and advisors to enrich our clients' service experience.

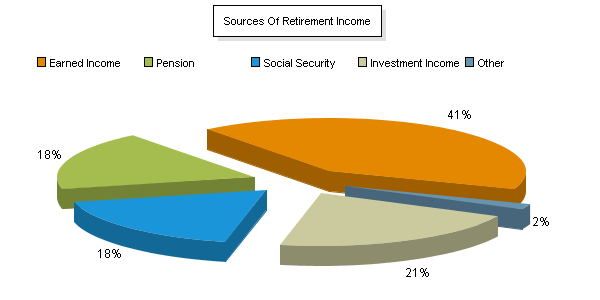

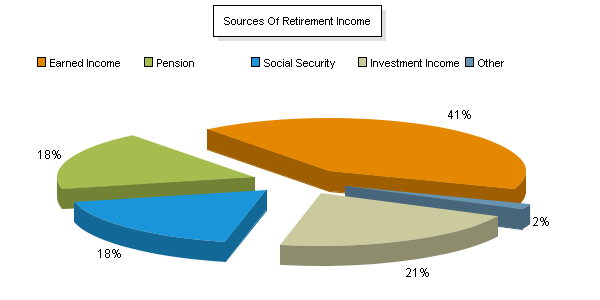

The United States Social Security Administration ("SSA") estimates that individuals depending upon Social Security as their only source of income will fall drastically short of their retirement income need.

At StateTrust, we work closely with our clients to develop retirement plans geared to achieving a desired standard of living during their retirement years.

The following image illustrates an estimate of income sources during retirement for people aged 65 years and older with an annual income greater than $51,165, as of February 2010.

Most Americans are Not Saving Enough for Retirement

The personal savings rate, defined as a percentage of disposable personal income, has been falling for more than 20 years in the United States and is recently just beginning to increase due to the economic recession of 2008-2009. Most people simply aren't saving enough for retirement.

The following image shows the U.S. personal savings rate since World War II (1947-2010).

Source: US Department of Commerce. Bureau of Economic Analysis.

How much money will be needed for retirement is a question that depends on each individual investor. StateTrust will help clients customize retirement savings and investment strategies to reach their retirement financial goals.

The following image illustrates the amount of monthly savings needed to reach $1 million by age 65 for various ages. Obviously, the earlier you start, the easier it will be to achieve your retirement savings goal, due to the power of compounding investment returns.

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.

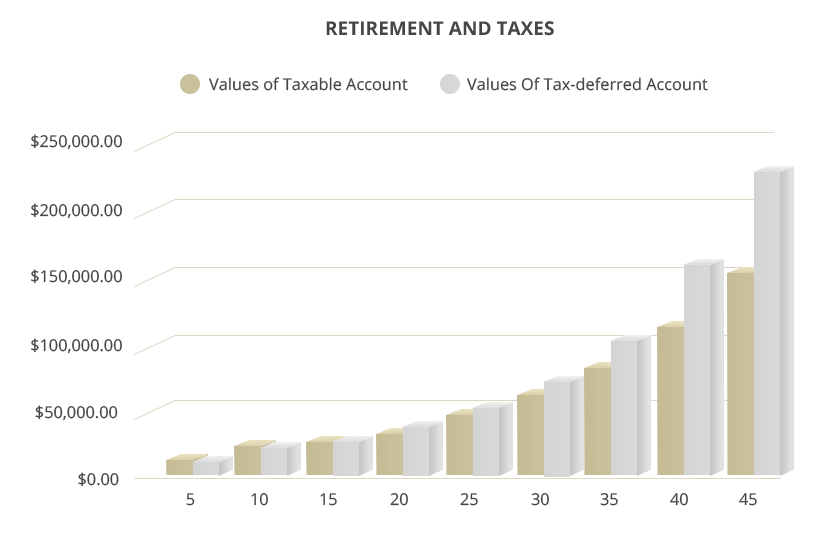

StateTrust financial advisors always take into consideration tax consequences when analyzing different financial strategies for our clients. While it is impossible for individuals to avoid taxes with most investments, it is often possible to defer taxes. Deferring taxes over long periods of time can result in substantial gains.

The following image illustrates how deferring taxes can increase the value of an investment over time, when a hypothetical value of $10,000 is invested in both a taxable and a tax-deferred account.

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.

Links of interest: