StateTrust's fixed income desk deals in all major regions of the world from the developed markets of the U.S. and Western Europe to emerging markets in Latin America, Eastern Europe, Middle East, Africa, and Asia.

Our Fixed Income desk can help clients trade more than 25,000 bonds from 90 different dealers and keeps them up-to-date with events happening in the fast-changing bond markets.

What is a Bond?

A bond is a debt security, in which the authorized issuer ("debtor") owes the holders ("lenders") a debt and, depending on the terms of the bond, is obliged to pay interest (the coupon) and/or to repay the principal at a later date, termed maturity. A bond is a formal contract to repay borrowed money with interest at fixed intervals.

Bonds can be issued in foreign currencies. Issuing bonds denominated in foreign currencies allow issuers to tap into investment capital available in foreign markets. Some foreign issuers look to diversify* their investor base away from their domestic market.

* Diversification does not guarantee a profit or ensure against loss.

Bond Valuation

The price of a bond is influenced by the following factors:

- Interest rate expectations.

- Current market interest rates.

- Maturity or length of the term.

- Creditworthiness of the issuer.

These factors are likely to change over time, so the market price of a bond will vary after it is issued. This price is expressed as a percentage of nominal value. Bonds are not necessarily issued at par (100% of face value, corresponding to a price of 100), but bond prices converge to par when they approach maturity (if the market expects the maturity payment to be made in full and on time) as this is the price the issuer will pay to redeem the bond.

Features of Bonds

| Features | |

|---|---|

| Principal Amount | The amount on which the issuer pays interest, and which, most commonly, has to be repaid at the end of the term of the bond. |

| Coupon | The contractual interest rate that the issuer pays to the bond holders. |

| Maturity | The date on which the issuer contractually has to repay the nominal amount. |

| Price | The price paid by an investor to buy the bond. Issue Price is the price paid when the bond is issued. |

| Interest Structure | The interest rate can be fixed or variable. Variable rates are typically linked to money market indexes such as LIBOR. |

| Quality | Credit ratings can provide a quality grading of certain bond issues. Investment grades bonds will have the best rating and junk bonds the worst. |

| CallabilityPutability | Some bonds give the issuer the right to repay the bond before the maturity date on the call date (callability). Other bonds give the holders the right to force the issuer to repay the bond before the maturity date on the put dates (putability). |

| Convertibility | Lets bondholders exchange a bond for a number of shares of the issuer's common stock. |

| Coupon Dates | The dates on which the issuer pays the coupon to the bond holders. In the U.S. and Europe, most bonds are semi-annual, which means that they pay a coupon every six months. |

| Indentures and Covenants | An indenture is a formal debt agreement that establishes the terms of a bond issue, while covenants are the clauses of such an agreement. Covenants specify the rights of bondholders and the duties of issuers, such as actions that the issuer is obligated to perform or is prohibited from performing. |

| Type | Description |

|---|---|

| Fixed Rate Bonds | The coupon remains constant throughout the life of the bond. |

| Floating Rate Bonds | The coupon is variable and linked to a reference interest rate such as LIBOR, Euribor or Prime. |

| Zero-Coupon Bonds | They pay no regular interest. They are issued at a discount to par value, so that the interest is effectively rolled up to maturity permitting the bondholder to receive the full principal amount on the redemption date. |

| Inflation Linked Bonds | The principal amount and the interest payments are indexed to inflation. |

| Asset Backed Securities | The interest and principal payments of these bonds are backed by underlying cash flows from other assets. |

| Perpetual Bonds | Also known as Perpetuities, these bonds have no maturity date. |

| Bearer Bonds | Are bonds represented by an official certificate issued without a named holder. In other words, the person who has the paper certificate can claim the value of the bond. Bearer bonds are very risky because they can be lost or stolen and are seen as an instrument to conceal income or assets for tax purposes. |

| Registered Bonds | Are bonds whose initial ownership (and that of any subsequent purchaser) is recorded by the issuer, or by a transfer agent. It is the alternative to a Bearer bond. Interest payments and the principal due upon maturity are sent to the registered owner. |

Categories of Bonds

Bonds can be categorized by Type of Issuer. There are generally two type of issuers:

- Corporate Bonds - These are bonds issued by companies. Large corporations have a lot of flexibility as to how much debt they can issue. Generally, maturities for short-term corporate bonds are less than five years; for intermediate bonds maturities range from five to twelve years, and for long term bonds maturities are usually over twelve years. Corporate bonds are characterized by higher yields because there is generally a higher risk of a company defaulting than a government.

- Government Bonds - These are bonds issued by a sovereign state. Depending on their maturities they can be classified as: Bills (debt securities maturing in less than a year), Notes (debt securities maturing in 1 to 10 years) and Bonds (debt securities maturing in more than 10 years).

Additionally, Bonds can be categorized by the geography or region of the Issuer. For example:

- Domestic Bonds

- International Bonds

- Emerging Market Bonds

- Asian Bonds

| US Government Securities | Description |

|---|---|

| Treasuries | Treasury Bills - These feature the shortest maturities—13, 26, and 52 weeks—and are considered as liquid as cash. Along with minimal credit risk, they also have minimal interest rate risk because they mature so quickly.

Treasury Notes - These mature between 2 and 10 years, which means that there is more interest rate risk and that their prices rise and fall more than Treasury bills. Treasury Bonds - Government securities with up to 30 year maturities. Zero-Coupon Treasuries - Also known as strips, these securities are the most volatile. Also, even though you do not get any interest payments, you will pay taxes as though you do. One way to take advantage of them is to buy them through tax-deferred accounts like Individual Retirement Accounts (IRAs). Treasury Inflation-Protected Securities - Known as TIPS, these securities are issued by the US Treasury department as a special kind of security whose principal amount is adjusted for inflation. The Treasury Department issues TIPS because it believes their issuance will reduce interest costs to the Treasury over the long term and will increase the different types of investors that buy their debt instruments. |

| Municipal Bonds | Municipal bonds, known as "Munis", are the next progression in terms of risk. Cities don't go bankrupt that often, but it can happen. The major advantage to munis is that the returns are free from federal tax. Furthermore, local governments will sometimes make their debt non-taxable for residents, thus making some municipal bonds completely tax free. Because of these tax savings, the yield on a muni is usually lower than that of a taxable bond. Depending on your personal situation, a muni can be a great investment on an after-tax basis. |

| Federal Agency Bonds | Federal agencies in the U.S. issue a massive amount of debt—in the trillions of dollars. Some of these Agency Bonds are:Fannie Mae - Bonds issued by the Federal National Mortgage Association (FNMA).

Freddie Mac - Bonds issued by the Federal Home Loan Mortgage Corporation (FHLMC). Ginnie Mae - Bonds issued by the Government National Mortgage Association (GNMA). Bonds issued by the Federal Farm Credit Banks Funding Corporation. Bonds issued by the Federal Home Loan Banks Office of Finance (FHLB). |

| US Series Savings Bonds |

Series EE Bonds - Are offered in 8 denominations ($50, $75, $100, $200, $500, $1,000, $5,000 and $10,000). They are purchased at 50% of their face value and are guaranteed to reach face value in 20 years.

Series I Bonds - Are offered in 7 denominations ($50, $75, $100, $200, $500, $1,000 and $5,000). They are purchased at face value. |

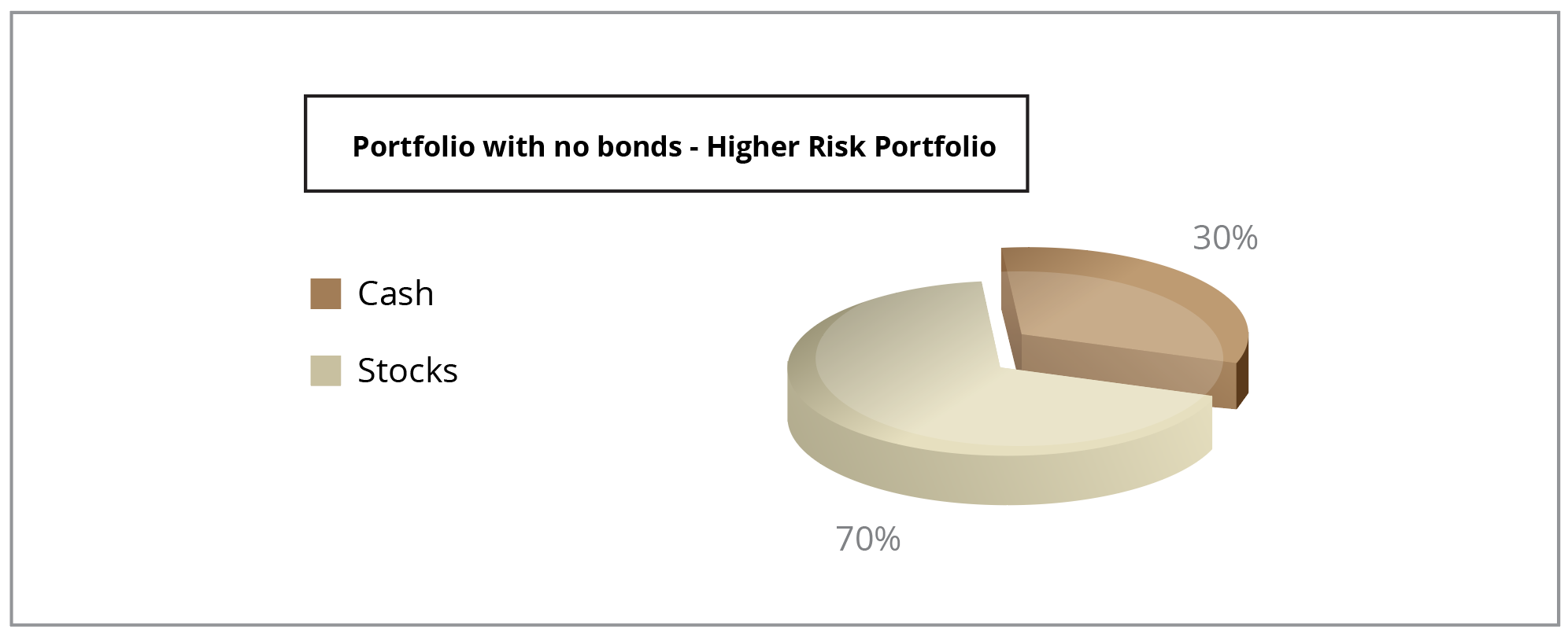

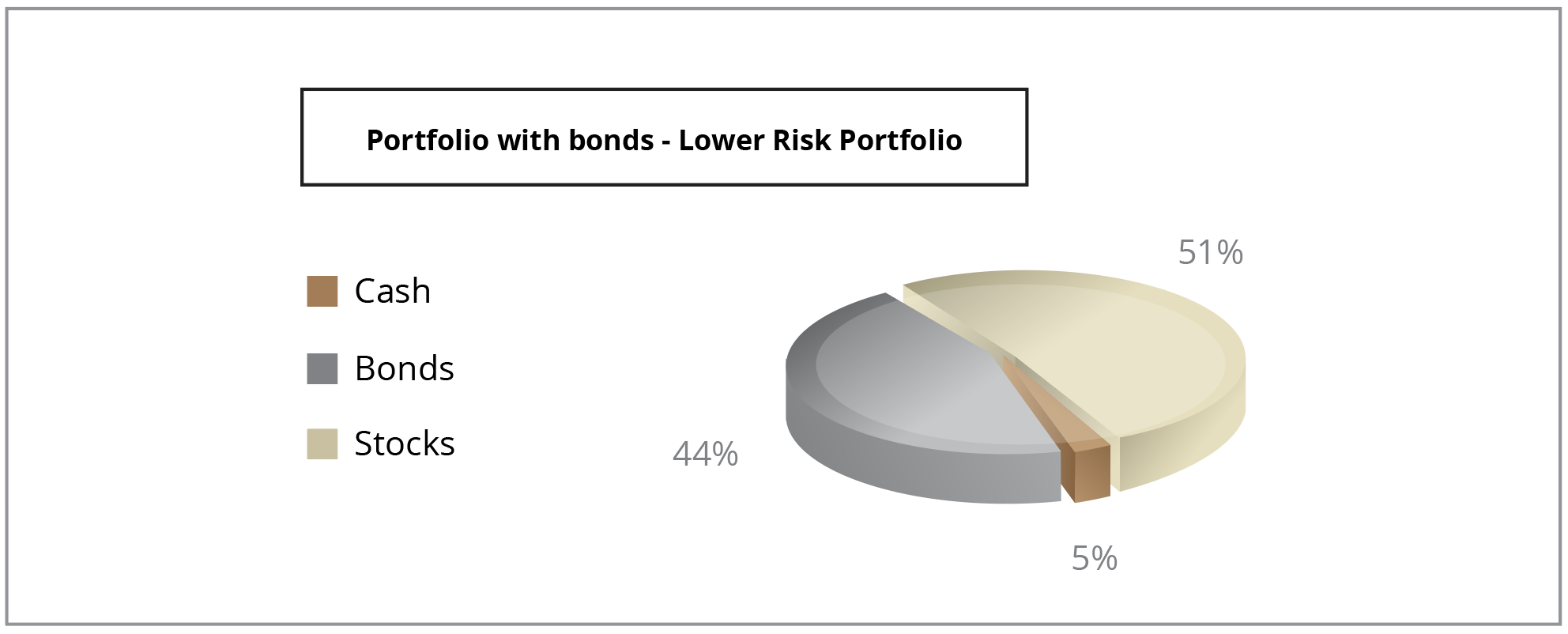

Adding a Bond Allocation to Diversify*

Historically, adding bonds to a portfolio comprised of stocks and cash equivalents has reduced portfolio volatility without sacrificing the level of return. This image illustrates the risk and return profiles of two hypothetical investment portfolios over a 40 year period (1971-2010). Although both portfolios had the same level of return, the portfolio containing bonds assumed less risk—meaning it experienced less volatility. The graph below illustrates that by diversifying* the original portfolio the overall risk of the portfolio was reduced without having to sacrifice the 9.8% return.

|

|

|||||||||

|

|

|||||||||

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.

* Diversification does not guarantee a profit or ensure against loss.

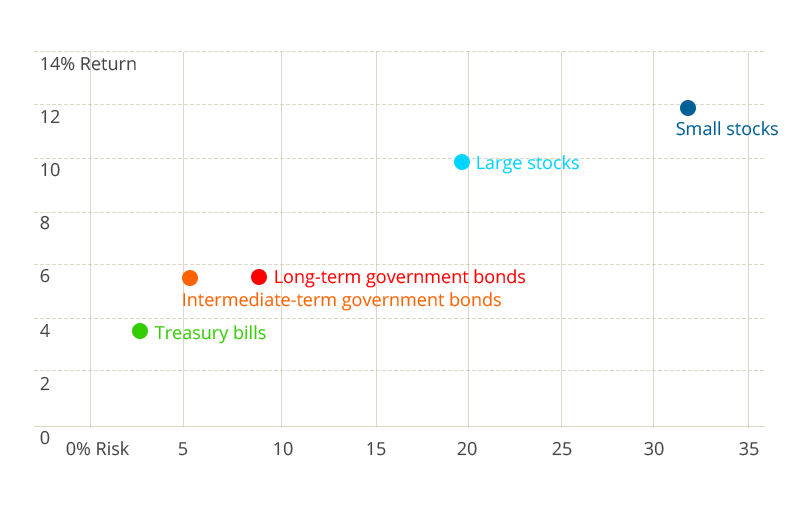

When developing a portfolio asset-allocation policy, it is important to understand the risk/return relationship of the assets being considered. The following image illustrates the risk/return relationship of five traditional asset classes over the period 1926 - 2010:

Source: StateTrust’s analysis of Morningstar data. Performance shown is not indicative of the performance of any specific investment. An investor cannot invest in an index, such as the one these graphs are based on. Past returns are no guarantee of future performance. These returns are based on historical information, from sources believed to be reliable, but accuracy cannot be guaranteed, and these returns can vary in future time periods.

Credit Rating Agencies

Rating agencies are private companies that measure the financial status and repayment capability of bond issuers. Ratings, quite simply, evaluate the probability that bond issuers will repay the principal and interest of bonds in full and on time. They are not recommendations on which bonds to buy and sell.

In the United States all of the ratings agencies are supervised by the Securities and Exchange Commission (SEC) which does not allow for conflicts of interest between rating agencies and the groups that they are rating.

Some of the top global Bond rating agencies are:

Rating agencies use four different elements to provide bond ratings:

- Capacity - The bond issuer's ability to repay the interest and principal on time.

- Character - Explores management's history, success with business plans, honesty, and operations.

- Collaterals - Assets used to back contractual debt.

- Covenants - Conditions the bonds were issued under—decide who gets paid back first in the event of a default and if the bonds can be called back.

Factors Affecting Bond Ratings

The quality of a Bond is influenced by a variety of factors. Some factors are directly dependent to the issuer's ability to meet its financial obligations and other factors are dependent on the issuers environment such as country regulations, currency and political environment. All these factors can cause a change in the bond's rating.

Important factors that are considered by rating agencies are:

- Economic fluctuations.

- Business climate.

- Company reorganization.

- Management restructuring.

- Tax increases/decreases.

- Revenue increases/decreases.

- Changes in the regulatory environment affecting the issuer.

- Net income changes

Bond Credit Rating System

| Risk Grade | Bond Grade | Moody's | S & P | Fitch | Meaning |

|---|---|---|---|---|---|

| Best Quality | Investment Grade Bonds | Aaa | AAA | AAA | Issuers exceptionally stable and dependable. |

| High Quality | Aa | AA | AA | High quality, with slightly higher degree of long-term risk. | |

| High-Medium Quality | A | A | A | High-medium quality, with many strong attributes but somewhat vulnerable to changing economic conditions. | |

| Medium Quality | Baa | BBB | BBB | Medium quality, currently adequate but perhaps unreliable over long-term. | |

| Speculative | Speculative Grade Bonds | Ba | BB | BB | Some speculative element, with moderate security but not well safeguarded. |

| Very Speculative | B | B | B | Able to pay now but at risk of default in the future. | |

| Poor Quality | Junk Bonds | Caa | CCC | CCC | Poor quality, clear danger of default. |

| Highly Speculative | Ca | CC | CC | Highly speculative quality, often in default. | |

| Lowest Rated | C | C | C | Poor prospects of repayment though may still be paying. | |

| In Default | - | D | D | In default. |

Bonds' credit rating movements are highly correlated with price movements in the same direction. That is, as credit ratings go down, they will pressure bond prices downward. Likewise, if credit ratings go up, they will push the prices upward.

Links of interest: